If you were to look at fintech apps at random, you’d quickly spot ones that help you collect your paycheck earlier, settle up IOUs and invest your money. If you spent a little more time digging, you might uncover banking apps designed for immigrants, Black Americans and the LGBTQ community. What you likely wouldn’t notice are products built for the formerly incarcerated. Until recently.

Stretch, an early-stage fintech startup, is now making the audience its sole focus in an attempt to win over a group of people who are up against all kinds of financial challenges, including securing work.

“Having spent 10-plus years in the industry, we saw a very overlooked demographic with so much need to get the right solution and service,” says Yasaman Hadjibashi, founder and co-CEO at Stretch and a former group chief innovation director at Barclays. “It has been literally unserved or underserved.”

If Stretch has its way, that is bound to change for the 600,000 or so individuals released from U.S. state and federal prisons every year.

Digital banking, job leads for individuals with criminal records

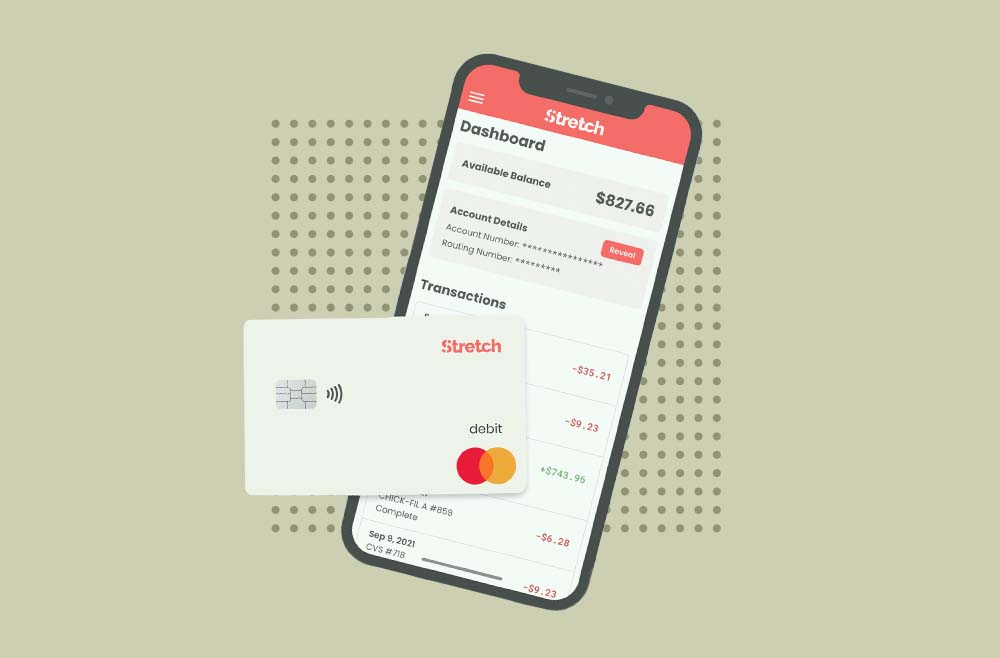

Right now, the Dallas startup partners with Evolve Bank & Trust to offer a no-monthly fee account with features you’d expect like debit cards and free ATM access. But the bank account is secondary to another feature in the web app: job leads at companies that hire individuals with criminal records.

“Yes, you have a free checking account, but the main thing is being able to find that job so you have a place to put that paycheck,” says Keith Armstrong, founder and co-CEO at Stretch, which works with Honest Jobs to collect job leads.

While more employers are open to hiring the formerly incarcerated given the tight labor market, these individuals are still up against much higher unemployment rates compared to the general population, and observers say it got worse during the pandemic. So the idea is for them to use Stretch as an antidote.

In October, Stretch started courting its first customers through a partnership with the Anti-Recidivism Coalition (ARC), a nonprofit in Los Angeles that helps the formerly incarcerated rebuild their lives across California. Stretch is one of the first challenger banks to pursue the demographic and its soft launch represents part of a larger trend of bank accounts becoming ever-more targeted to help underrepresented groups.

It won’t be the last.

A grant for nonprofit-fintech partnerships seeking to help the formerly incarcerated

Stretch and the ARC are among the 2021 grantee winners of a program run by the Financial Health Network’s Financial Solutions Lab. The program is currently focused on projects designed to help individuals with conviction histories. Another partnership grantee, Mobility Capital Finance and the Urban League of Essex County, is working on a mobile banking solution to help returning citizens and their families in New Jersey. Other nonprofit-fintech partnerships have paired to work on solving the community’s problems like building credit and navigating debt disputes. Separately, the First Step Alliance is creating a nonprofit to help the formerly incarcerated achieve financial freedom.

The projects point to a major gap in the financial system.

“This is a particular sub-population that faces really challenging and pressing barriers to accessing financial services and is paying substantial costs when it comes to financial health,” says Hannah Calhoon, vice president of innovation at the Financial Health Network.

Upon release, one immediate obstacle is obtaining a government ID to prove identity. While some individuals have access to their records like birth certificates, thanks to family support during their sentences, not everyone will.

Others come home after decades with no paperwork and it takes quite a lot of traveling to the DMV without a car, in transitional housing, with a curfew and with no cellphone.

— Rachel Chungdirector of development at ARC

The challenges don’t end there. Dealing with identity fraud or catching up on technology, like email and social media if their sentences were longer, are common obstacles. Those are in addition to paying fines and fees related to their convictions and potentially dealing with wage garnishment for an old debt, like child support.

“It’s not one particular barrier,” says Amelia Josephson, a manager of the Financial Health Network’s Lab. “It’s a set of barriers that folks need to have addressed when looking for banking access.”

‘When they come out, they are unbankable and they don’t know why’

Many formerly incarcerated people need bank accounts when they’re released because their financial institution dropped them while they were locked up from inactivity or from the balance dropping below zero.

When the Office of Financial Empowerment started working with financial institutions in 2015 to help more than 100 formerly incarcerated individuals secure a bank account, the Lansing, Michigan-based agency saw the problem repeatedly.

“So many of them had dish network contracts, cellphone contracts, things that were coming out of their account automatically,” says Amber Paxton, director of the Office of Financial Empowerment. “If they had that and then, let’s say, they left $300 in their checking account and they became incarcerated, well pretty soon, those monthly charges are going to eat up what’s left in the checking account. It will eventually go negative. Now they have a ChexSystem record. When they come out, they are unbankable and they don’t know why.”

Some formerly incarcerated individuals may never have had an account before, either. According to research from the Financial Health Network, 29 percent of justice-involved respondents were unbanked prior to incarceration.

Of course, not everyone wants a bank account.

“Players in the industry have not bothered targeting them as part of their strategy,” Stretch’s Hadjibashi says. “But individuals, the end customers themselves, may have some mistrust toward financial institutions overall that stops them from wanting to go to a bank and open a bank account right away.”

But Stretch is betting it can overcome the perception problem by forming partnerships with organizations that have already earned the community’s trust (like the ARC) in addition to providing features that help individuals access income sources.

It doesn’t make the startup’s quest easy, of course. To become a successful challenger bank, you will face all kinds of obstacles. For Stretch, its target market presents added complexities. For example, its audience struggles with identity challenges all of the time, including having theirs stolen while in prison, which could interfere with getting an account later. Right now, Stretch requires a Social Security number, residential address, email address and phone number to become a customer — a driver’s license is not part of its standard sign-up process.

How will Stretch make money?

Figuring out how to make money from a client base who may have very little to start is another looming obstacle. For example, individuals who are released from prison in Texas are given $50 checks and a bus ticket when released and another $50 check when they report to their parole officer. Inmates in Texas don’t earn an hourly rate for work they do in prison (except those in special programs). On the other hand, they might have some savings. Family members can deposit money into an inmate trust account, while others may have earned money as part of a work release program.

“We’ve talked to some people who have $6,000 saved up at the time of their release,” Armstrong says. “It’s all very much a case-by-case basis.”

Regardless of their starting point, Stretch plans to earn revenue from collecting interchange fees when someone swipes its debit card. In time, it plans to diversify the way it makes money. For example, its customers may rely on family and friends to get to and from work, if not the local bus. Auto lending could be an opportunity for a future premium service. “Helping people get access to a reliable ride is something we are exploring,” Armstrong says.

Just the beginning for Stretch

For the coming months, Stretch plans to remain focused on collecting feedback from its initial customers to make sure its product is solving the community’s initial financial plight.

Over time, Stretch imagines a future where its customers “stretch” their earning potential, from say, working in a warehouse to earning a three-figure salary as a truck driver because of using its app. If and when they progress, these individuals will have a collection of savings options at their fingertips.

Already, the desire of the community to build wealth is evident.

“One thing we have learned about the demographic is they are very entrepreneurial and very ambitious,” Armstrong says. “A lot of people just ended up selling the wrong product.”

Learn more:

Credit: Source link

{kind=link}