- The following is a panel recap from our “On the Road @ Money 20/20” coverage in Las Vegas.

- The session unpacked the what banks can learn from working with fintechs.

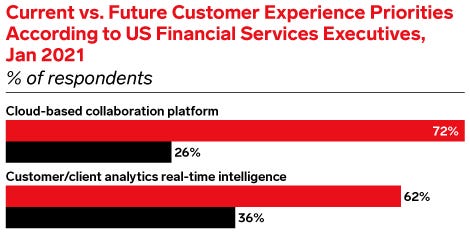

- Insider Intelligence publishes hundreds of research reports, charts, and forecasts on the Banking industry. Learn more about becoming a client.

Session Name: “How to Modernize Legacy Infrastructure While Transforming Traditional Cost Structures”

Speakers:

- Jesse Wedler, partner at CapitalG, moderator

- Erin Erhart, executive VP at Midwest BankCentre

- Laura Spiekerman, founder and owner, Alloy

- Nathaniel Harley, co-founder and CEO, Mantl

Findings: Before technology can transform banking, banks must overcome the challenge of the legacy infrastructure that “they are stuck with,” said Jesse Wedler, a partner at CapitalG.

Insider Intelligence

Legacy infrastructure is the No. 1 hindrance to digital innovation in banking. Nathaniel Harley, co-founder and CEO of Mantl, stated that 43% of banks still use systems written in COBOL.

Harley said the number of banks is projected to halve over the next 10 years, noting that “if you don’t transform your bank, you face an existential risk.” But there’s hope in technology, he added: “Banks have great stories to tell when they have the right tools to compete and can partner with vendors to have a Chime-like or Chase-like experience.”

For most banks, “ripping and replacing and starting fresh,” as Wedler put it, isn’t an option. The time, money, and risk of reputational damage from a technology failure is too daunting. “From a cultural perspective, most banks aren’t ready to take that on,” Harley said.

Partnerships with fintechs and legacy core systems coexisting with a digital “wrapper” on top are more likely. This lets banks bring in best-of-class solutions and gives them a lot of the value offered by modern core systems.

What This Means: The session unpacked the digital transformation of Midwest BankCentre, a community bank established in 1907 in St. Louis, Missouri. Midwest executive VP Erin Erharr shared what the bank learned from working with fintechs.

- Community banks are particularly reliant on core systems, and their “level of comfort with doing things differently can be low,” Erhart said.

- For a community bank, saying, “Hey, we’re not going to have signature cards or use photo IDs” was a big step, she noted. Change can threaten a bank’s identity, so creating a culture of change was critical.

- For a tech initiative to succeed, it’s important for banks to understand what problem it’s trying to solve. Midwest put a lot of thought into how to support growth by reworking its deposit strategy, seeking flexibility in its branch footprint, and appealing to a younger demographic that often overlooks community banks.

- Selecting the right vendor was key. When vendors under consideration spoke of simply moving a manual or physical process online, “the demo would stop right there,” Erhart said. The bank wanted a vendor with vision for a seamless transaction that was fully digital.

- Laura Spiekerman, founder and owner of Alloy, said fintechs need to spend a lot of time educating banks—for example, by running tests in parallel to prove that a variety of data sources from Alloy might be as good or better than what the bank’s core provides.

- Erhart cautioned banks against “lowering the bar” on their digital aspirations—it could prevent them from finding that best-in-class vendor willing to spend time educating the bank, as Spiekerman described.

- Banks also need to shift from seeing tech as a cost center. Spiekerman said: “When they’re viewing it as an investment and not looking for the cheapest way to launch a digital project, they do the best work.”

- Erhart compared due diligence in technology investment to what’s needed when building a branch. “There’s a reason for placement in that community and a goal for breakeven and profit. The same goes for technology.”

Our Take: Smaller US banks start out at a technological disadvantage compared with their larger counterparts. US small and medium-sized financial institutions (FIs)—defined as those with less than $100 billion in assets—have small budgets for technology that make it harder for them to recruit talent, per Insider Intelligence.

To keep their digital offerings competitive, small and medium-sized FIs have three options: They can 1) build new products internally, 2) combine with other banks to pool resources, or 3) partner with outside vendors.

Teaming up with third-party companies like Alloy and Mantl can be the most efficient of the three choices, as vendors have already developed resources and are ready for quick deployments.

Want to read more stories like this one? Here’s how you can gain access:

- Join other Insider Intelligence clients who receive Banking forecasts, briefings, charts, and research reports to their inboxes each day. >> Become a Client

- Explore related topics more in depth. >> Browse Our Coverage

Current subscribers can access the entire Insider Intelligence content archive here.

Credit: Source link

{kind=link}