WASHINGTON — For years, federal regulators have struggled to set parameters for the inclusion of fintechs in the banking system. Some experts say the clearest-cut solution may be to revamp the National Bank Act.

Policymakers looking to create specialized charters for nonbanks have shied away from the legislative process. But the Office of the Comptroller of the Currency’s special-purpose fintech charter, for example, which would bestow banking powers without the need to accept deposits, has been slowed by legal disputes.

Most recently, the Biden administration is reportedly exploring the creation of a specialized charter for stablecoin issuers. But observers say that idea could similarly be held up by years of litigation unless Congress acted more decisively to authorize it.

“I don’t see how you could do that without a change in the banking laws, and that raises fundamental questions,” V. Gerard Comizio, an associate director at American University’s Washington College of Law, said of the creation of a stablecoin charter.

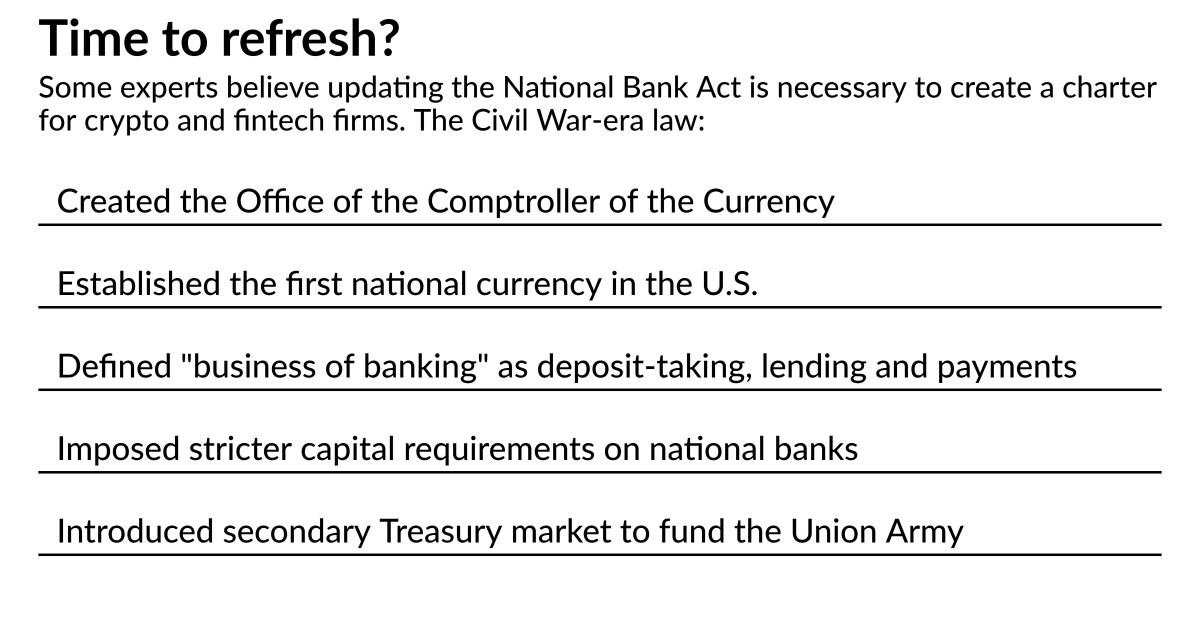

The National Bank Act, first passed in 1863 and amended in 1864, created the OCC and established the activities that make up the “business of banking” for nationally chartered banks. Those are understood today to be receiving deposits, making loans and facilitating payments.

The OCC has claimed the law authorizes limited-purpose bank charters for fintech firms that only do some of those functions, such as a nonbank lender that does not accept deposits. Such an option would preclude the need for Federal Deposit Insurance Corp. approval.

But state regulators have stymied the OCC’s charter plans in court, arguing that the federal agency’s interpretation exceeds its authority under the NBA.

As technology transforms the financial system and brings new entrants to banking’s door, many suggest it is time to redraw boundaries in the federal banking system and that that effort should go through Congress.

Through the OCC’s actions, key components of the National Banking Act have already been “stretched and expanded and added to and loopholed in so many ways that it has no bearing on its original intent,” said Mehrsa Baradaran, a banking law professor at the University of California, Irvine.

“If it has risk like a bank, it should be regulated like a bank,” Baradaran. “And Congress should decide what kinds of risks we are worried about and which regulator should be in charge of those risks.”

To be sure, 11 years after the passage of the Dodd-Frank Act, Congress is unlikely to have much interest in comprehensive banking reform, especially without the motivating event of a financial crisis.

“They absolutely should fire up that furnace of legislative reconstruction of federal bank regulation and federal financial regulation. I think that they probably, absolutely won’t,” said Thomas Vartanian, executive director of the Financial Technology and Cybersecurity Center, a nonprofit foundation. “What will happen is just another bandaid stuck on an obsolete structure of financial regulation, which actually could make it worse rather than better.”

But Baradaran said Congress would have the power to reset rules of the road at a pivotal time in the world of banking.

“Congress created the OCC and the [Federal Reserve] and the [Federal Deposit Insurance Corp.],” she said. “Congress is the power that can change them if they wish.”

Since the summer, financial regulators have been meeting through a Presidential Working Group to develop an oversight approach to cryptocurrencies.

Those recommendations are expected to be published in a report later this month. But some initial approaches under consideration have already begun to leak out through the press. Earlier this month, the Wall Street Journal reported that the Biden administration may urge Congress to bring up legislation creating a tailored charter for crypto firms.

“The proposal seems to pre-suppose that the OCC would become the federal regulator in the driver’s seat on virtual currency regulation,” said Comizio.

If a new crypto framework runs through the National Bank Act, Congress could take the opportunity to retool the “business of banking” clause and address those legal questions, either clarifying the OCC’s ability to allow activities-based bank charters or, on the opposite end of the spectrum, restricting the agency’s discretion significantly.

Some observers say the focus on crypto firms and other types of fintechs looking to compete with banks is similar to decades ago when securities firms began offering money-market instruments and other types of products to mimic bank offerings.

“This is another moment that has a lot of parallels for me going back to the 1970s and ‘80s, where new types of institutions are trying to get into the banking industry and, to some extent, banks are trying to get into their businesses as well,” said Arthur Wilmarth, professor emeritus of law at George Washington University.

“You have to think — what do we think the banking business really consists of at its core?” Wilmarth said.

Meanwhile, the OCC has tried to introduce a special-purpose charter for fintech firms since 2015. The charter would allow fintechs to do only a limited number of activities as defined by the “business of banking,” which could lower a firm’s overall regulatory burden. If a fintech sought a charter to do lending but not take insured deposits, it could theoretically avoid direct supervision by the FDIC.

State authorities have spent years battling the OCC in court over the charter, arguing that the National Bank Act does not give the federal regulator the legal authority to offer bank charters on an à la carte basis.

But revising the NBA could offer more legal clarity, some observers say, and more flexibility with a broader view of what defines banking. Critics note that a narrow definition results in traditional depository institutions losing significant market share to less regulated nonbanks.

“We have myopically regulated bank charters, simply because they’re banks and have deposit insurance, while most of the risk in the financial services system has moved to areas that are not prudentially regulated,” said Vartanian.

It’s an old truism in policy circles, however, that financial legislation rarely appears in the absence of a financial crisis.

“Crypto generally and stablecoins specifically are moving ahead rapidly. This is the engine that should be a catalyst for dynamic legislative change,” said Vartanian. “The problem is that Congress isn’t going to do anything unless there are enormous sea changes in competition, or a cataclysmic crisis.”

Not everyone agrees that the relationship between new bank legislation and a full-blown crisis is ironclad, however. In a forthcoming paper from the University of Pennsylvania’s Peter Conti-Brown and New York University’s Michael Ohlrogge, the authors found that “crisis legislation can account for only half or less of total legislative importance in banking.”

“The crisis legislation hypothesis fits strongly for securities laws, but far less so for banking legislation,” Conti-Brown and Ohlrogge wrote. “We conclude, therefore, that reformers would be ill-advised to only push for government interventions in the banking system post-crises.”

If Congress does manage to buck that trend, some observers say the financial services sector could broadly benefit. “It’s in everyone’s interest to get in front of legislation that takes in both the industry’s view and the regulators’ view to get to a balanced approach for all parties,” Comizio said.

But the road to that point could be long.

“This is a complicated issue, and it could absolutely involve overhauling a lot of financial laws and regulation,” Comizio said. “The bottom line is that there is no federal law that was written with bitcoin in mind.”

Credit: Source link

{kind=link}