Leadership changes at Rocket Cos. are part of a strategy to not only become the nation’s biggest provider of purchase mortgages in 2022, but to convince investors that they should think of Rocket and its growing stable of more than a dozen brands as a fintech platform.

Based in Detroit, Rocket Cos. is a holding company for a stable of personal finance and consumer technology brands that employ 26,000 people, including Rocket Mortgage, Rocket Homes, Rocket Loans, Rocket Auto and Amrock.

Jay Farner

“We’re going to be able to show investors yes, you’ve got this high upside of [mortgage] origination revenue, but you’ve also got all this other consistent revenue that you can think about year in and year out,” Rocket Cos. CEO Jay Farner said at one of two year-end investment conferences where he honed that message. “And as we tell that story, I’m very hopeful that we’ll start seeing our company trade more in the fintech multiple that we believe it deserves.”

Rocket’s biggest business, Rocket Mortgage, made the most of record low mortgage rates seen during the pandemic. As homeowners rushed to refinance, Rocket funded $320 billion in mortgage loans in 2020, more than double the company’s 2019 total of $145 billion.

But since going public in an IPO priced at $18 per share in August, 2020, shares in Rocket Cos. have been on something of a roller coaster ride, briefly trading for above $40 in March 2021, and recently touching an all-time low of $13.69 this week.

At 4.72, Rocket’s current trailing price-to-earnings ratio is an order of magnitude lower than those enjoyed by many fintech companies during 2021, reflecting investors’ concerns that with mortgage rates now on the rise, Rocket’s mortgage refinancing business — and profits — will wane.

Not only is lining up homebuyers who need purchase loans harder than refinancing existing loans, but purchase loans are typically less profitable. Although Rocket posted its best quarter ever for purchase loans during the three months ending Sept. 30, net income was down 53 percent from a year ago, to $1.39 billion.

To counter the narrative that Rocket’s profits will continue to slip, Farner has staked out an ambitious goal: Rocket will seek to surpass rival Wells Fargo and become the number one retail provider of purchase mortgages in the next 12 to 18 months.

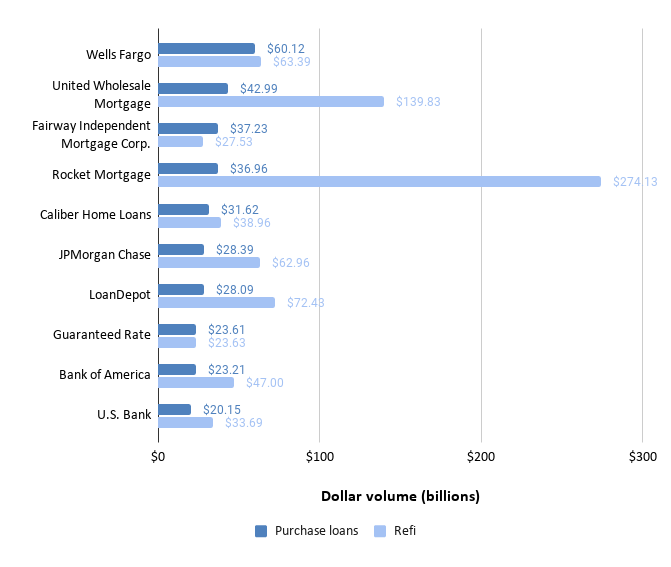

Top 10 mortgage lenders by 2020 purchase loan volume. Source: iEmergent.

Farner says Rocket can achieve that goal not only because its technology gives it an edge, but because the Rocket family of companies has access to consumers through multiple channels, including real estate agents, insurance agents, banks and credit unions.

Leadership changes

Rocket started off the New Year by announcing leadership changes across several of its businesses, which it said were aimed at increasing connectivity throughout the platform.

In addition to his duties as Rocket Cos.’ CEO and vice chairman, Farner has served as the CEO of Rocket Mortgage, Rocket’s biggest source of revenue and profits.

In a move that drives home his message that Rocket is a fintech platform, Farner is giving up his role as CEO of Rocket Mortgage to head up Rocket Central, the centralized hub for the Rocket Cos. fintech platform.

As CEO of Rocket Central, Farner “will drive the vision for the technology, data, product design, marketing, communications and other services the company provides – ensuring there is a consistent, seamless experience for clients across the Rocket Companies ecosystem,” the company said.

Bob Walters

Farner is handing off his Rocket Mortgage CEO duties to Bob Walters, a 25-year veteran of Rocket Mortgage. Walters, who has overseen mortgage servicing, client experience operations, capital markets and technology at Rocket Mortgage, will continue to serve as president and COO of Rocket Cos.

Tim Birkmeier

Rocket Mortgage Chief Revenue Officer Tim Birkmeier, who joined the company in 1996, will broaden his responsibilities by also assuming the role of president. Birkmeier oversees all teams and initiatives that create top-line revenue, including mortgage banking and the partnership channel.

Nicole Beattie

Rocket had previously announced in November that 17-year Rocket Mortgage veteran Nicole Beattie, the company’s executive vice president of mortgage servicing, would succeed Brian Hughes as CEO of Amrock, Rocket’s title insurance, property valuations and settlement services subsidiary.

LaQuanda Sain

After Beattie assumed the role of CEO at Amrock on Nov. 19, LaQuanda Sain was promoted to lead Rocket Mortgage’s servicing team, which collects payments on more than $521 billion in mortgages held by 2.5 million clients, generating $1.3 billion in recurring servicing fee income on an annualized basis.

‘The original fintech company’

In addition to becoming the nation’s largest retail provider of purchase mortgages, Farner has set the ambitious goals of growing Rocket’s share of the overall mortgage market to 10 percent in 2022, with a long-term target of 25 percent market share.

To do that, Rocket will not only continue to invest in technology that’s made it the nation’s leading mortgage lender, but harness the collective power of companies under the Rocket umbrella to reach consumers through multiple channels, Farner said.

At the Credit Suisse 25th Annual Technology Conference in December, Farner told Credit Suisse analyst Tim Chiodo that Rocket’s mission “since the mid-90s was leveraging technology, and then the internet, to grow our business.”

Chiodo agreed that, “in many ways, Rocket is the original fintech company.”

In explaining Rocket’s current approach to technology, Farner made a point of differentiating between consumer-facing front end apps and websites — where he conceded “we’ve seen a lot of people catch up to us” — and the back end framework where loan applications are processed, and decisions are made.

“Real fintech is about the backend platform,” Farner said. “It’s about the way that we’re able to move data and information to drive efficiencies. For our business, it allows us to process, underwrite and close mortgages at a lower cost than our competitors. So we can dedicate more dollars towards marketing and things that grow our business, which is why we’ve had such incredible growth these last 20 plus years.”

Farner said Rocket was able to double loan production at the outset of the pandemic as homeowners rushed to take advantage of low mortgage rates, without going on a hiring spree.

“I think a true Fintech is about building out that technology platform that drives great efficiency and great scale to your business,” he said.

“When you go from being the largest mortgage lender in the country at $145 billion, and boom, you double the number of loans you’re closing, we certainly didn’t double our staff in three weeks. It was the technology that brought that scale. And I think that’s how for us at least we measure what a true fintech is.”

Farner said Rocket began thinking about mortgage lending as a workflow management opportunity “15, 20 years ago.” To stay ahead of the competition, Rocket has 3,000 employees devoted to developing new technology in house. Last year, the company piloted Rocket Logic, an automated underwriting system designed to close loans faster by leveraging data and asking dynamic questions.

“We are now building technology … that allows us to think about this as a point-of-sale decisioning process,” Farner said. By “leveraging all the data that we’ve got, we’re talking about knowing that that loan is going to close the day you originate that loan. And that backend technology, I think, puts us years ahead of our competition.”

The impact of Rocket’s backend technology is multiplied by the many channels through which the company can reach consumers — including a “pro network” of real estate and insurance agents who can originate mortgages on Rocket’s platform, he said.

“When they call their insurance agent saying, ‘Hey, I’m ready to buy a home,’ that insurance agent can originate the loan,” Farner said. “When they call their Realtor, and the Realtor says, ‘You should use Rocket’ — or, in some cases, the Realtor says, ‘No problem, I’ll use Rocket and originate the loan.’ We’re right there at the point of sale.”

Farner said all of this adds up to the “real secret” behind Rocket’s growth potential — “the lifetime value of the client.”

“In the mortgage business, you spent a lot of time reacquiring a client,” he said. Building a platform that offers different products and services “allows you to engage clients. So if we do some marketing that brings in a first time homebuyer that’s 12 or 24 months away from purchasing, we can keep them engaged, bring value to them, so we go ahead and capture that client. That platform — I don’t see anybody really building out a true Amazon of fintech the way that we are.”

The acquisition of Truebill

Another example of how Rocket is focusing on the lifetime value of the clients it acquires is the company’s pending $1.27 billion acquisition of personal finance app Truebill. The acquisition, announced in December, represents another opportunity to market real estate services, mortgages and other loans to Truebill’s 2.5 million members.

Rocket spends about $1 billion a year in marketing, and Farner said it gets more bang for the marketing buck when it expands , Farner told told Ryan Nash, managing director of equity research at Goldman Sachs at another year-end conference.

“One of the things that we have the opportunity to leverage is the incredible marketing that we already do,” Farner said. “I used to use an analogy, ‘We’re buying this fish and we’re just taking one piece of the filet. But there’s so much else, let’s harvest all of that opportunity.’ And so we don’t have to spend more marketing dollar to do that. And that’s why we’re adding on these additional services that bring real value to our clients that are hard, complicated.”

Truebill helps consumers manage subscriptions, budgeting and spending, and when scouting for acquisitions, “We typically pick things that are challenging, that we think we [can] do better than others,” Farner said.

The purchase loan growth strategy

Rocket doesn’t break out exactly how much of its mortgage lending business is refinancing, and how much is purchase loans. But Farner did reveal that “somewhere close to 60 percent of all our origination volume is not rate sensitive.” Included in that figure are both purchase mortgages and cash out refinances, which, unlike “rate and term” refis, can make financial sense even if the borrower can’t get a lower interest rate.

Rocket’s real estate brokerage and search subsidiary, Rocket Homes, already plays an important role in the company’s purchase loan growth strategy, Farner said.

“We’ve got millions of people visiting the website, looking at MLS listings,” Farner told Chiodo. “We’ve got our thousands of [partner] real estate agents in the field that are working with clients because we trust them. We know they’ll provide a great experience. We’ve got our centralized real estate portal that we’re building out so we can service clients at a lower fee [in house].”

Rocket Homes, which had obtained real estate brokerage licenses in all 50 states in order to operate a property search site and agent referral network, announced last summer that it planned to hire on-staff real estate agents and launch an iBuyer program “throughout the remainder of 2021 and into early 2022.”

Farner said he also sees an opportunity “to really lean into” Rocket’s ForSaleByOwner.com business.

“If you study the current purchase market, you could make an argument that 15 percent or 20 percent of all transactions should be for sale by owner transactions.”

Farner has high hopes for a partnership with Salesforce, announced in October, which allows Rocket to offer its mortgage technology to 10,000 banks and credit unions that originate $1 trillion in mortgages a year through Salesforce Financial Services Cloud.

Salesforce is “great at selling their software into these banks and credit unions, Farner told Nash. “We’ve now given them another strong value add to their software, but they’re actually now out there selling for us.”

Farner said Salesforce CEO Marc Benioff told him that his team “is very excited … to sell this software, to be able to talk about bringing this service to these banks and credit unions.”

Key Rocket Cos. subsidiaries

Rocket Cos. has evolved from a single mortgage lender to an ecosystem of businesses involved in home financing, home sale and search, personal finance, auto sales, media, and client services and technology solutions.

Companies under the Rocket umbrella include:

- Rocket Central: A centralized hub for the Rocket Cos. fintech platform, providing technology, accounting, legal services, public relations and human resources. Formerly known as Rock Central.

- Rocket Mortgage: After claiming to have created the “the first fully digital mortgage experience” in 2015, when it was known as Quicken Loans, Rocket Mortgage grew to become the nation’s largest mortgage lender with $320 billion in loans originated in 2020.

- Rocket Homes: Real estate brokerage and search portal that allows consumers to search multiple listing service data for homes, connect with a real estate professional and obtain mortgage approvals through Rocket Mortgage.

- ForSaleByOwner.com: Online marketplace enabling consumers to buy or sell properties on their own, offering financing through Rocket Mortgage.

- Amrock: National provider of title insurance, property valuations and settlement services, “preferred provider” to Rocket Mortgage.

- Amrock Title Insurance Co.: Nationwide title insurer, providing underwriting services for national title insurance agent, Amrock.

- Rocket Loans: Online personal loan company that takes applications online, with funding provided by partner Cross River Bank as soon as the same day.

- Rocket Auto: Virtual marketplace where consumers can shop for cars offered by a network of dealers.

- Truebill: Consumer finance app that tracks spending and helps users budget and build up their credit score.

- LowerMyBills.com: Online comparison service for mortgages, credit cards, insurance, loans, home services and personal finance.

- Core Digital Media: Digital, social and display advertiser generating leads for mortgage, insurance and education providers.

- Nexys Technologies: Software solutions for streamlining, digitizing and automating mortgages processes.

- Rock Connections: Sales and support platform providing contact center services including appointment setting, prequalifying clients, lead and efficiency consulting, lead generation, reporting and analytics.

- Rocket Innovation Studio: Recruits and mentors technology talent to support the needs of Rocket Companies.

- Woodward Capital Management: Issuer of private label mortgage-backed securities, providing funding for loans originated by Rocket Mortgage.

- Lendesk: Canadian mortgage technology provider of products to digitize and simplify lending.

- Edison Financial: Canadian digital mortgage firm that employs Lendesk’s Spotlight as its lender submission platform.

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

Credit: Source link

{kind=link}